Peloton

Not enough credit is given to Bill Ackman for his Chipotle investment back in 2016. The situation had similarities to the AMEX salad oil scandal - a great company with near-term solvable problems (in CMG’s case, an ecoli outbreak; in AMEX’s case, guarantees outstanding related to a corporate fraud).

When he announced the position, people haaaaated his math and logic.

But the end result? >50% annualized returns (though Pershing Square has pared its stake along the way). Equally importantly to being right, it was a big position (9.9% of the company, almost 20% of the fund).

Today, I think that the situation at Peloton has some interesting comparisons to Ackman’s Chipotle investment.

I. Peloton: the History, Brand, and Tread Disaster

Peloton enjoyed incredible growth until the pandemic, when things really took off:

But then Peloton launched the Tread, a treadmill extension of their signature bike, which was the equivalent of an e coli outbreak.

Short summary, after a number of injuries and one child death, Peloton fought with the Consumer Product Safety Commission to try to avoid a recall, only to have to reverse this stance shortly thereafter and issue one. Whoops:

On the day that they announced the Tread recall, Peloton lost $4 billion in market cap.

But Peloton got through it and re-launched the Tread in August (random tangent - I don’t know why they didn’t rebrand this product upon the relaunch. Doesn’t matter how good the name Tread was.).

Recently, they launched their private label apparel brand.

Seemingly, they were getting back on their feet after the Tread disaster. Only Q3 was too early to show any positive results; rather, it still showed the legacy problems including higher expenses and the forward guidance was reduced to reflect more muted (but still strong) growth. The stock sold off huge.

That’s the opportunity.

II. Valuation

I bought a Peloton bike a few years ago and love it - it’s great for a quick workout when I don’t have more than 30 minutes to spare, it’s motivating, and I like the competitiveness of the leaderboard. I’m not a fanatic, but I get 2-3 workouts per week on average on my bike when I’m not traveling. I don’t know anyone who owns a Peloton and doesn’t rave about it.

An example of the love of the product: Scott Galloway once wrote, “There are over 250,000 members of the wildly popular Official Peloton Member Facebook page. These people post 23 times per hour and interact with each other through comments and likes.” 18 months later, that same Facebook group has 850,000 members.

But the stock, after hitting a high of ~$160 per share, has been a disaster. Today, it’s trading at levels not much higher than where it was prior to the beginning of the pandemic:

I find that last sentence unreal: that a company which permanently benefitted from the work-from-home dynamics of the COVID-19 economy and that has rapidly grown its subscriber in 18 months is trading at the same levels as February 2020. Just crazy.

Absent the unforced error relating to the Tread (that might have been avoided had management read a case study of Johnson & Johnson and the Tylenol scandal of the early 1980s), I imagine the valuation would still be 2-3x what it is today.

But I don’t see these issues stopping it from getting back there over time. Rather, growth continued despite all of these problems and the reopening of the economy.

Peloton is now forecasting growth and a return to profitability in 2H FY 2022, despite the ~20% lower Bike prices.

Further, now that they raised some capital, there’s no immediate concern about a cash crunch (I didn’t think the raise was necessary given that there should have been some working capital tailwinds in December, but regardless it’s helpful because it eliminates any concerns). Risks have been mitigated substantially along with the decline in the share price. Seems like a winning combination.

III. Ideas for Growth & Community

Acquisitions

Peloton’s most recent acquisition was a supplier of exercise equipment to vertically integrate (in line with Galloway’s T Algorithm), but there are a few other acquisition candidates which could help accelerate its brand and mission. Most obvious from my perspective is On Running, which would add a new product layer (footwear) and which is already aligned with two of Peloton’s new markets (apparel and the Tread).

Personal view: On would be a natural extension for Peloton (albeit crazy expensive at On’s current valuation). Emphasizing this point, check out the super-cool combined logo:

I hope there’s a young, hungry banker out there somewhere who’s pitching this idea.

Social / Creator Expansion of Platform

I wonder if Peloton would consider adding a social / creator aspect of its platform - for example, allowing certain members to host classes (and these member/creators could get compensated based on how many people take their class). I would think there would be all sorts of ways to segment this from the main platform to avoid diluting the instructors’ brands (live classes only - no recordings; must be friends to join a hosts class; additional subscription fee required to become a member/creator, etc). For a company that thrives on its community, this seems like it could be an interesting way to keep people active and engaged, and would also make the Peloton community more local. I think it might be a cool idea, no clue whether or not it would it work work. This would also enable celebrity-hosted classes???

Cutting Prices

I can think of two other times when a luxury product with an adamant fan base was cutting prices to spur additional demand - Apple & Tesla. There were critics to both of those bull cases as well. I missed both of them like an idiot…and I also missed Chipotle when Ackman bought in after the ecoli outbreak… I have no intention of making those same mistakes again.

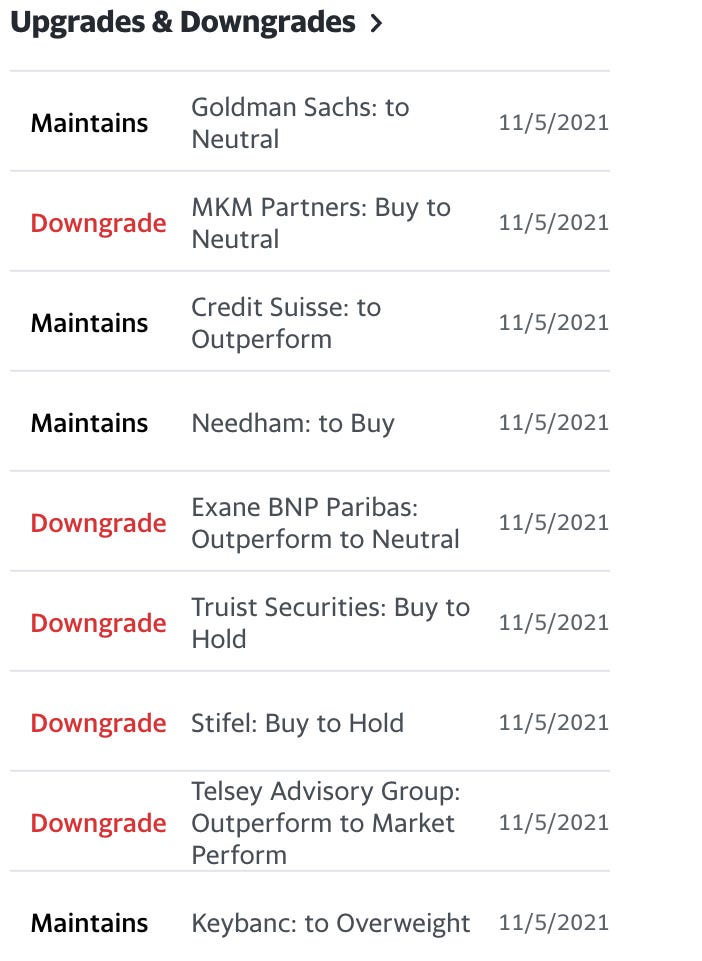

IV. The Sell Side

A bit of a tangent: on this week’s episode of “the Sell Side is hysterical”: 5 sell-side firms downgraded PTON after their earnings release, after the stock was already down 66% from its highs. Funny.

V. Conclusion

For all of the reasons above, I think PTON is a solid long-term investment at these levels.

I briefly looked into the convertible notes, but given that they are so far out of the money (>$200 strike price) and with only a ~4% current yield, they didn’t seem worth the mitigated reward / risk.

Therefore, we’ve initiated a small long-position (shares). Though of course I am confident - now that I have written this position publicly (and solely for that reason) - that it’s going to sell off further. I’ll plan on adding if it does.

Sherwood Ltd.

November 19, 2021

Disclosure

Sherwood Ltd. has prepared this report with the expectation that anyone reading this analysis isn’t foolish enough to think that it is anything other than an opinion that is held at the time of writing. This isn’t investment advice. Rather, Sherwood Ltd.’s investment advice is for you to read Burt Malkiel and invest monthly in a diversified low-cost index fund over a long period of time.

In no event shall Sherwood Ltd. or the author(s) of this report be liable for any claims, losses, costs or damages of any kind, direct or indirect, arising or in any way connected with this report. Any actions you take are at your own risk. Sherwood and the author(s) of this report have no intention on updating as to when and if they close out any positions or change their investment theses.

Hopefully there are no material errors in this analysis, but if there are, we would appreciate if you would contact us so that we may correct them. Even better if you can change our minds with your different perspective and facts which we may not have seen in the course of our research.