Canoo Inc. & Shorting Horses

I haven’t spent much time looking into SPACs, though I know a few people who have made a lot of money in the space. From a personal perspective, I’ve really enjoyed the sector; for example, I have found the various bearish reports on SPACs from Nate Anderson (Hindenburg Research) & others to be great entertainment.

In one article about Hindenburg’s Nikola short, there was a reference to a company that I had never heard of: Canoo Inc. (NASDAQ: GOEV). So I decided to take a brief look.

Canoo is an Electric Vehicle SPAC that went public in December 2020. GOEV currently has a market cap of ~$1.8 billion, even though its shares are below where they were when the transaction closed:

There have been a few bearish articles on Canoo. For example, in May 2021, Edwin Dorsey of the Bear Cave published a brief short report, mainly focused on executive departures, related party transactions and alleged mismanagement:

But here’s my favorite piece of information that Dorsey didn’t include: Canoo publicly disclosed in its financial statements that it doesn’t expect to ever commercially produce a vehicle.

Not an encouraging sign for shareholders…And there are other red flags as well.

I. Background on Canoo Inc.

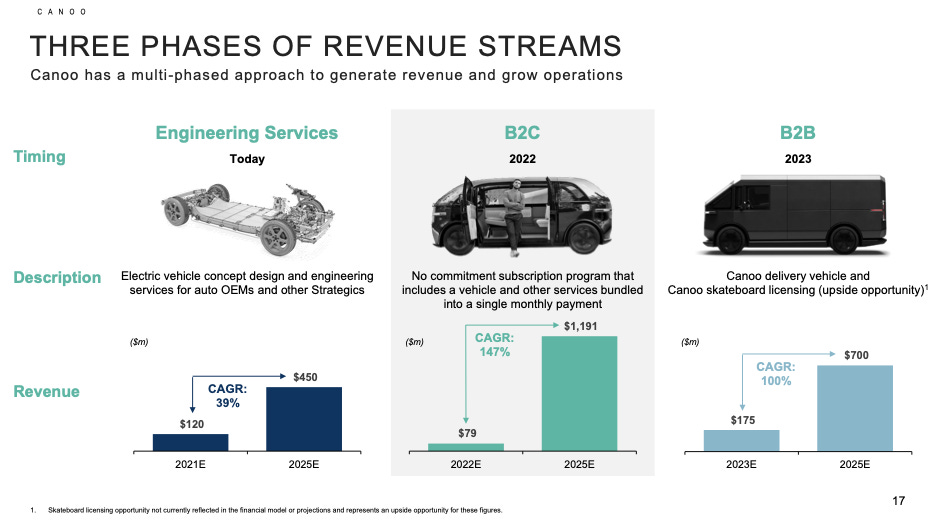

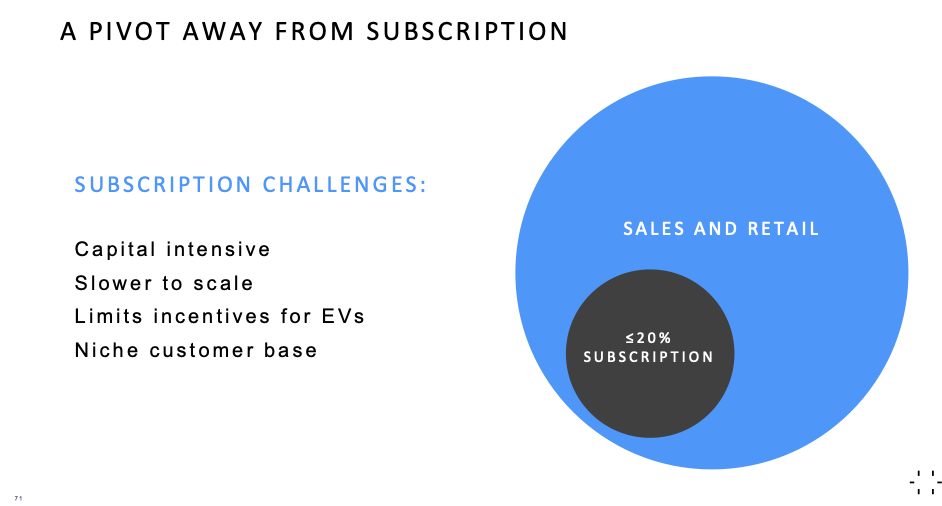

Canoo merged with Hennesy Capital Acquisition Corp IV on December 21, 2020, and started trading on December 22, 2020. At the time of the transaction, the original business model was to manufacture EVs and then offer them on a subscription basis, wherein customers would pay a single monthly price for a Canoo vehicle (minimum one month subscription), alongside offering engineering services to other auto OEMs:

This initial business plan had numerous challenges. To start, it was very capital intensive (i.e. the company had to finance manufacturing the car and would only earn the subscription proceeds on a monthly basis) and subscriptions seemingly didn’t qualify for any EV tax incentives (which are only available for a purchase of an electric vehicle). Further, it’s not apparent that consumers have any interest in a subscription service for a car compared to other alternatives (ownership, leasing, etc.). These issues were highlighted in the following slide from Canoo’s June 2021 Investor Day:

But there was initial excitement about the technology and the platform – for example, in February 2020, Canoo had announced a partnership with Hyundai wherein Hyundai would use Canoo’s “skateboard technology” (which is in essence a modular chassis for EVs).

By March 2021, just four months after its SPAC transaction, Canoo pivoted its from its subscription-based business plan to focus instead on fleet sales and the “Canoo Ecosystem.” Around the same time, the partnership with Hyundai – which was the foundation for its “engineering services” revenue stream - was cancelled.

II. Disclosure on Commercial Production Expectations

As mentioned above, Canoo publicly disclosed in its financial statements that it doesn’t expect to commercially produce any vehicles. Specifically, when valuing its restricted stock awards, the company stated:

“50% [of the awards] vest on the date the Company starts commercial production of its first vehicle, which the Company determined was not probable of being met as of December 31, 2020.”

This reference appears again (word for word) in both the Q1 2021 and Q2 2021 reports.

Amusingly, in December 2020, the managements’ RSA vesting schedule was changed from the milestone trigger upon commercial production to a time-based trigger:

On December 18, 2020, Legacy Canoo approved an amendment to change the [commercial production of first vehicle] vesting goal of all eligible Founder Restricted Shares held by Legacy Canoo’s executives to time-based vesting with a merger trigger, which was satisfied on December 21, 2020. The investor-held Founder Restricted Shares’ [commercial production of first vehicle] vesting goal was not amended. The amended time-based vesting of the [commercial production of first vehicle] portion has a cliff vesting of 25% on March 18, 2020 with the remaining shares vesting quarterly over 36 months thereafter. The amendment was accounted for as a grant modification in December 2020.

Maybe more amusingly, about a month after the initial 25% cliff vesting of the remaining RSAs, the various corporate resignations referenced by Dorsey started (which ultimately would result in the CEO, CFO, General Counsel and Head of Corporate Strategy all leaving within a short period).

III. A Little Better Product

I love this quote from Elon Musk about new products:

“If you’re a new company, unless it’s a new industry or new market...if you’re entering into anything that’s an existing marketplace against large, entrenched competitors, then your product or service needs to be much better than theirs. It can’t be a little bit better.”

With this in mind, I don’t see how Canoo is pursuing a product that is more than just a little better (if at all). Regardless of whether or not you like the look of the product (personally, I think they’re wildly unattractive – though admittedly, I can’t claim to have a good sense of style or taste), it’s not clear what the real competitive advantages versus the competitors are.

Auto manufacturing is a business that is extremely difficult to operate in under the best of circumstances. Supporting this statement: thousands of automobile manufacturers in the US have gone bankrupt since the industry began (seemingly leaving an industry success rate of <5%).

One of my favorite Buffett quotes is:

“What you really should have done in 1905 or so, when you saw what was going to happen with the auto is you should have gone short horses. There were 20 million horses in 1900 and there's about 4 million now. So it's easy to figure out the losers: the loser is the horse. But the winner is the auto overall. 2000 companies (carmakers) just about failed.”

I don’t see the EV manufacturing space as any different. There are many other [better capitalized] competitors in this space vying for market share. This includes Tesla & Rivian, not to mention the multi-billion dollar auto companies such as Ford, Daimler, VW, General Motors, etc.

I can’t clearly see how Canoo vehicles beat out the other players in this extremely competitive marketplace.

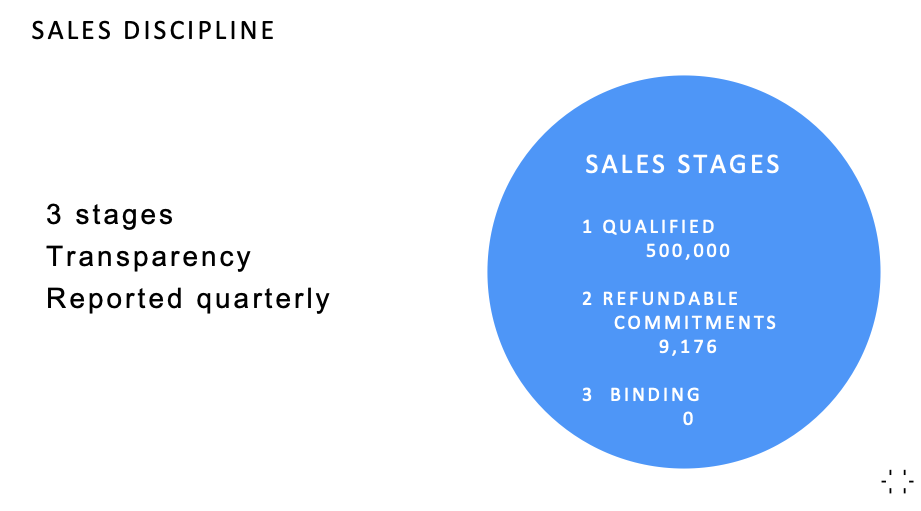

IV. Refundable Commitments

Canoo reported to have over 9,500 refundable commitments, but the refundable commitment is only $100. They have no binding orders.

These refundable commitments increased ~4% in from the last reported figures (from 9,176 to >9,500), generating ~$35,000 in cash. But the date of the 9,176 preorders disclosure was their investor day on June 17, 2021, and there is no comparison date for the 9,500 preorders disclosure in the Q2 report. If the 9,176 was from March 31, 2021 and the >9,500 from June 30, 2021, or in the alternative if the 9,176 was from June 17, 2021 (the date of the investor day) and the >9,500 was from August 16, 2021 (when they reported Q2, 2021), it represents approximately a ~4% quarterly sequential increase. That’s difficult to get excited about, especially when there is no indication of what the conversion rate will be to full purchases, nor any detail on who the preorders came from (Canoo added >100 employees in Q2 2021 and >200 YTD – how many placed a preorder?).

V. Cash Requirements

The company is burning through cash and it looks highly probably that GOEV will need to do additional dilutive financings:

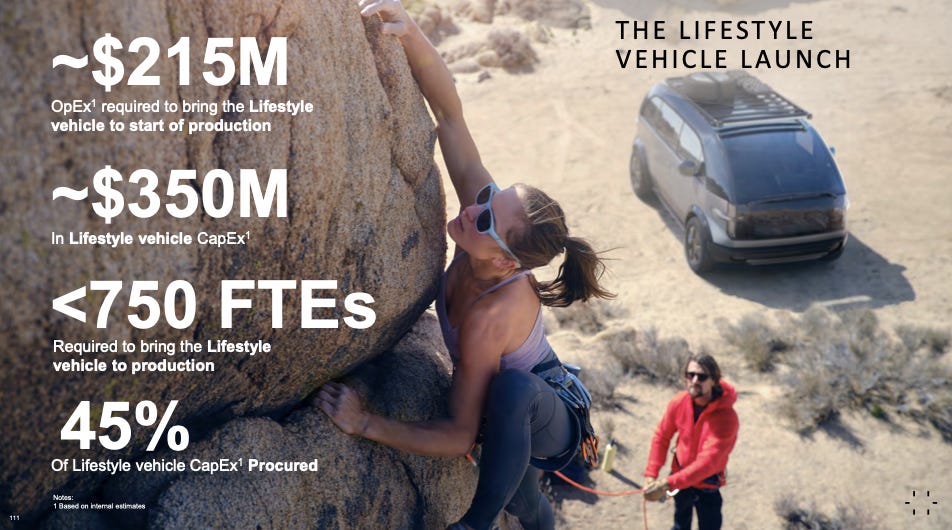

At its Investor Day in June 2021, Canoo stated that they needed $350 million in capex and $215 million of opex to get to vehicle production of their “lifestyle vehicle”

Rule of thumb is usually that expectations for these projects are less expensive and faster than reality. Further, it’s not clear what is included in the opex numbers. - i.e. whether or not other corporate overheads (for example, the ~US$1 million for reimbursement to the CEO for personal aircraft usage in the first six months of FY2021) are included. In addition, it appears they are spending a lot of money on other projects as well (the delivery van, the software, etc.). Therefore, it appears likely that a cumulative expenditure of well in excess of $565 million over the next 24 months is required.

Current cash on hand is $564 million, though it seems that GOEV can raise another ~$250 million if warrant holders exercise (exercise price is $11.50, v. ~$7.50 price today). Any cash from the warrant exercise won’t come in without the share price increasing dramatically.

Current cash burn rate (before any material capex) is ~80 million per quarter (stock based comp is an additional $45 million per quarter), and this will increase as they hire more people. However, including capex, GOEV guided the cash drain to be $120-140 million for Q3 2021.

If, on 12/31/21, GOEV has less than a year of forecast cash on hand (or if they don’t raise capital prior to finishing their audit in Q1 2022), they would be at risk of a going concern note in their financial statements. A quick look at another EV Startup, Lordstown Motors, should be sufficient for GOEV to want to avoid this situation at all costs.

Therefore, we currently would expect a dilutive financing to occur in the next 6-12 months.

This is also inferred in the Q2 10-Q:

“As a result, we will require substantial additional capital to develop our EVs and services and fund our operations for the foreseeable future. We will also require capital to identify and commit resources to investigate new areas of demand. Until we can generate sufficient revenue from vehicle sales, we expect to primarily finance our operations through commercialization and production with proceeds from the Business Combination, including the proceeds from the PIPE financing that took place concurrently with the Business Combination, and, as needed, secondary public offerings or debt financings. The amount and timing of our future funding requirements, will depend on many factors, including the pace and results of our research and development efforts and our ability to successfully manage and control costs.”

VI. SEC Investigation

On April 29, 2021, the SEC opened an investigation into the company for “the public offering and merger, operations, business model, revenues, revenue strategy, customer agreements, earnings and other related topics, along with the recent departures of certain of the company’s officers.” Never a positive sign.

It’s impossible to forecast whether or not this investigation will lead anywhere. Personally, I’m not expecting this to have any material impact on the company or its business, though it’s an important item to keep an eye on.

VII. Software Strategy

In Q1, Canoo announced the “Canoo Ecosystem”, which plays on the idea that every person that purchases a Canoo car will add a phone app and connect a device that gives them information about their other cars, such as tire mileage, service appointments, etc. They say it’s “an app store for vehicle owners”, but it’s not clear that the product is readily monetizable, nor that it will result in a competitive advantage in any material way to selling Canoo vehicles. If anything, it seems like an interesting - though unproven - concept for a standalone software application.

Consumer retail mobile app development is a very different business from EV manufacturing. In many ways, this looks like a distraction from what should be the sole focus of the company – producing cars. I don’t get it.

VIII. Material Weakness

Canoo had a material weakness with a major accounting error related to the sponsor warrants & related disclosure in 2020 (as did many SPACs), then another one in Q1 2021 (for a misstatement related to warrants / options). They announced their intentions to completely upgrade their accounting system and personnel related to this to avoid it in the future (presumably a major cost which will increase the cash burn).

I’ve said this before - every company has internal control deficiencies, though continuing material weaknesses (especially if they are constantly changing) can be a red flag.

Canoo’s material weakness was still outstanding as at Q2 2021:

“While we have made meaningful progress on strengthening our internal controls relative to the previously identified material weaknesses, those material weaknesses have not yet been fully remediated. Our management, with the participation of our Principal Executive Officer and Principal Financial Officer, evaluated the effectiveness of our disclosure controls and procedures as of the end of the period covered by this Quarterly Report on Form 10-Q. Based on that evaluation, our management concluded that our disclosure controls and procedures were not effective, at the reasonable assurance level, as of the end of the period covered by this Quarterly Report on Form 10-Q, as a result of the ongoing remediation associated with the material weaknesses both discussed below and identified in our Annual Report on Form 10-K and Quarterly Report on Form 10-Q for the quarter ended March 31, 2021.”

IX. Funny Slides in Presentations

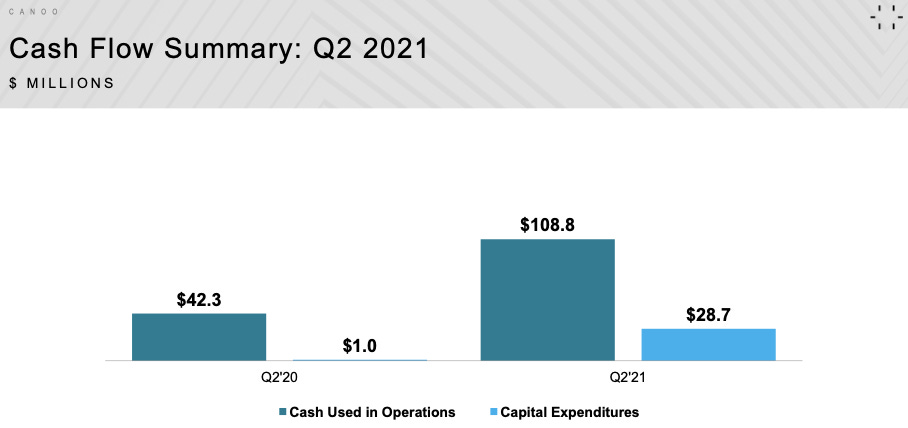

In their Q2 2021 presentation, Canoo decided to show Adjusted EBITDA as a negative number and net loss as a positive number. While this is technically correct, it seems like a strange PowerPoint decision that could be considered deceptive (they are both losses, why aren’t they both negative?):

In the same presentation, and in the same light, they showed cash used in operations as a positive number instead of a negative number. Again, while this is technically correct, higher cash used in operations is, all else equal, a bad thing, yet this chart looks positive (hockey stick up & to the right). If you didn’t look at the small legend at the bottom of the slide, you’d think that this company was printing cash. Strange.

X. The Positives

It’s not all negative – in just the last few months, GOEV has made progress and entered into two important agreements – the first, an agreement to build a manufacturing plant in Oklahoma with $300 million of non-dilutive financial incentives; and second, an agreement with VDL Nedcar, a Dutch multibillion dollar automobile manufacturing company, to produce vehicles until the Oklahoma facility is completed.

These are undoubtedly positive steps for the company.

But it’s still a very steep hill to climb, and I don’t believe that this changes the bear thesis. I’m sure there are other positives as well (patents, IP, etc.), though given the apparent headwinds, I can’t see them offsetting the negatives.

XI. Valuation

If the company’s disclosure from its RSA awards is correct, there appears to be at least a >50% probability that the business is worthless (if the company can’t commercially produce a vehicle, it will – in all likelihood - go under). If GOEV does execute well and succeeds in getting to commercial production, it enters a wildly competitive space with a product that doesn’t appear to be more than “a little bit better”, at best.

In response to Buffett, I’d argue that the 2,000 auto companies that failed were equally good shorts as the horse (if not better, because there were more of them).

Given the above, the various management turnover and issues identified by Edwin Dorsey, the execution risk on getting production up and running on time and on schedule, and the substantial quarterly cash losses which seem probable to result in future dilutive financings (maybe even in the very near term), we think GOEV is an attractive short candidate. We believe that there is an interesting argument to be made that its shares will eventually trade below $1.

That said…the trade is expensive and the shares are down huge over the last few months (apparently we’re late to the game and not alone in our thinking). This makes the risk / reward only moderately attractive, in our view. So we’ve initiated what we refer to as an “academic position” and will keep monitoring the file in case it becomes more economic in the future. Luckily, I am confident - now that I have written this position publicly (and solely for that reason) - that the share price is going to increase further. I’ll plan on adding if it does.

Sherwood Ltd.

September 2, 2021

Disclosure

Sherwood Ltd. has prepared this report with the expectation that anyone reading this analysis isn’t foolish enough to think that it is anything other than an opinion that is held at the time of writing. This isn’t investment advice. Rather, Sherwood Ltd.’s investment advice is for you to read Burt Malkiel and invest monthly in a diversified low-cost index fund over a long period of time.

In no event shall Sherwood Ltd. or the author(s) of this report be liable for any claims, losses, costs or damages of any kind, direct or indirect, arising or in any way connected with this report. Any actions you take are at your own risk. Sherwood and the author(s) of this report have no intention on updating as to when and if they close out any positions or change their investment theses.

Hopefully there are no material errors in this analysis, but if there are, we would appreciate if you would contact us so that we may correct them. Even better if you can change our minds with your different perspective and facts which we may not have seen in the course of our research.